Now that we have used the lease test to identify operating vs. finance leases, it’s time to calculate the “right-of-use asset” and lease liability that will be included on the balance sheet. The lease liability is equal to the present value of the remaining lease payments. To determine this:

First, determine the lease term.

Next, calculate the total lease payments over the lease term.

Finally, discount these payments using the appropriate discount rate to calculate the present value.

How do I calculate the lease term?

As noted above, the first step in calculating the lease liability, is to determine the term of the lease. The term is the total amount of the time between the commencement date and the ending date of the lease. The term may include periods covered by a renewal option, if it is reasonably certain a renewal option will be exercised.

How do I calculate the lease payments?

Next, we need to calculate the lease payments. In order to do this, we must break down the components of the lease agreement to understand what to include and what not to include. Once we have identified all of the lease components, we must then determine which will be included and those we will ignore in our calculation. And, finally, we perform the actual calculating!

First, let’s break down the components of the lease agreement.

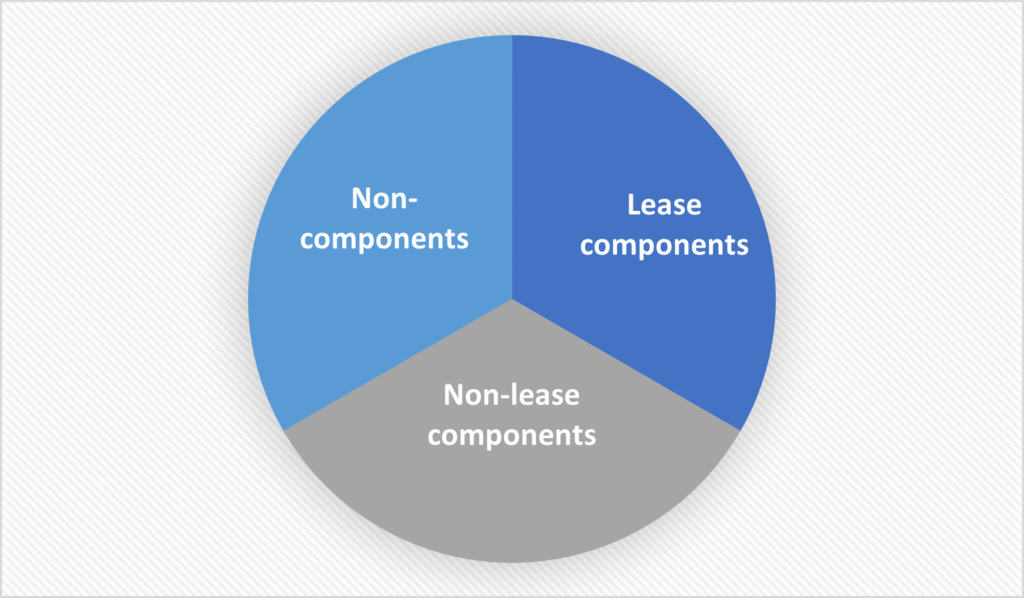

ASC 842 requires entities to identify the separate lease components within a contract.

Lease Components:

The entity shall consider the right to use an underlying asset to be a separate lease component if both of the following criteria are met:

The lessee can benefit from the right to use

The right to use is not highly dependent on or highly interrelated with other right(s) of use

Non-Lease Components:

Components of a contract include only those items or activities that transfer a good or service to a lessee. An example of a non-lease component in a contract might be charges for common area maintenance.

ASC 842 requires lessees to allocate the consideration in the contract to the lease and non-lease components.

The lease components are included in the lease payment calculation

The non-lease components are excluded in the lease payment calculation

Non-Components:

What about other items noted in the lease agreement, such as reimbursements for insurance or administrative tasks? According to ASC 842, these are not components of the contract. As such, they should be excluded from the lease payment calculation.

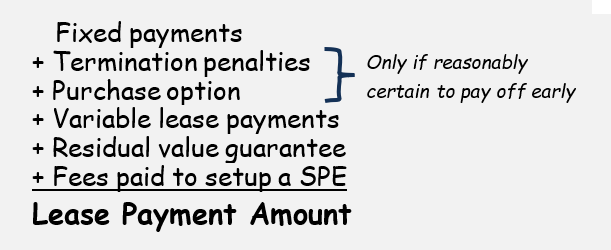

Calculating Lease Amount

Now that we have identified the different components of the lease payment, let’s calculate the lease amount.