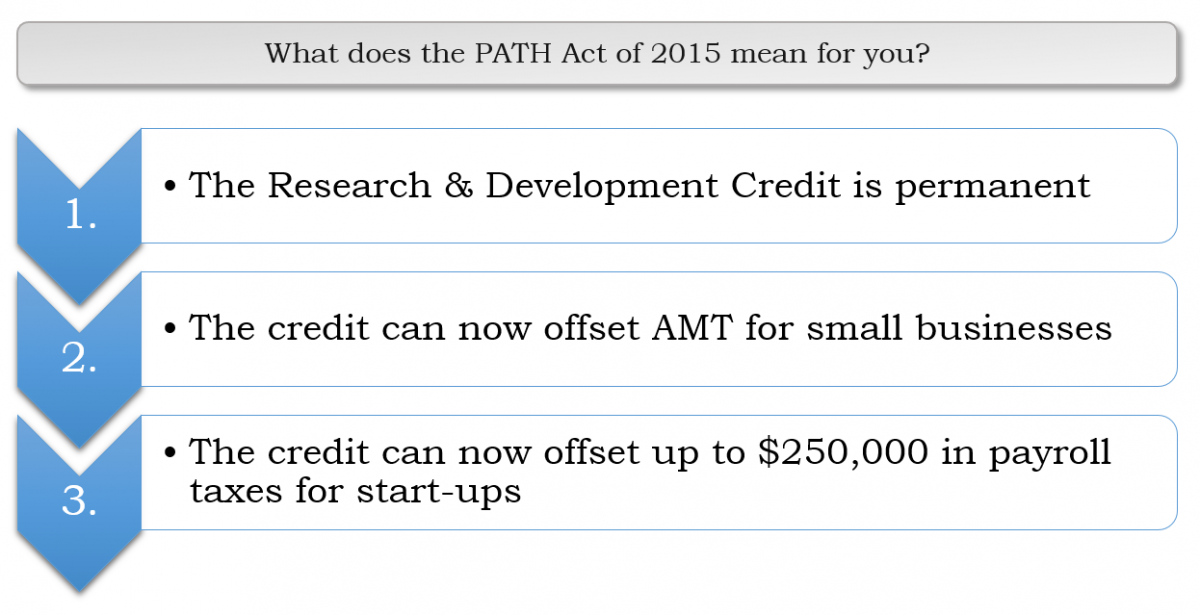

The Protecting Americans from Tax Hikes (PATH) Act of 2015 was signed by the President on December 18, 2015. One of the most significant provisions of the law was to make the Research and Development tax credit permanent. Although the research credit has been a part of the federal tax landscape since 1981, the law has had a series of expiration dates which required Congress to pass a new law to extend the credit. In fact, since the research credit's original expiration date of December 31, 1985, the credit has expired eight times and has been extended fifteen times.

The PATH Act now makes the research credit permanent and removes the periodic uncertainty that has surrounded it. This allows taxpayers to properly plan for these expenditures in anticipation of receiving the related tax benefits.

In addition to making the research credit permanent, the PATH Act also contains favorable changes for small businesses and start-ups beginning in 2016. These noteworthy enhancements include:

- Ability to offset AMT: The credit is now available to offset the Alternative Minimum Tax for eligible small businesses. These are taxpayers with less than $50 million in gross receipts. The AMT limitation has often caused taxpayers to lose the benefit of the research credit. The limitation was repealed for the year 2010, but was included in subsequent extensions of the research credit. For 2016 and forward, this limitation is lifted.

- Ability of offset payroll taxes: In the past, start-ups have not been able to utilize the research credit due to lack of taxable income. Another enhancement of the provision would allow both qualifying corporations and partnerships can now apply the credit to offset up to $250,000 in payroll taxes beginning in tax years after December 31, 2015. For these purposes, start-up companies are defined as taxpayers with less than $5 million in gross receipts in the current year and less than five years of historical gross receipts.