The year isn't over yet, but if your Company is off to a rough start, know that a silver lining may exist in the net operating loss (NOL) deduction.

The rules

A net operating loss occurs when a business's operating expenses and other deductions for the year exceed its revenues. To qualify for the deduction, you must have business expenses in excess of your business income, though certain modifications apply.

Generally, once you incur a qualifying NOL, you can either carry back the NOL as far as allowable (typically two years) and then carry forward any remaining amount, or you can elect to carry forward the entire loss. Carrying back a loss can generate an immediate tax refund, which could free up cash flow during a difficult time. Carrying forward a loss will offset income for up to 20 years in the future.

For example

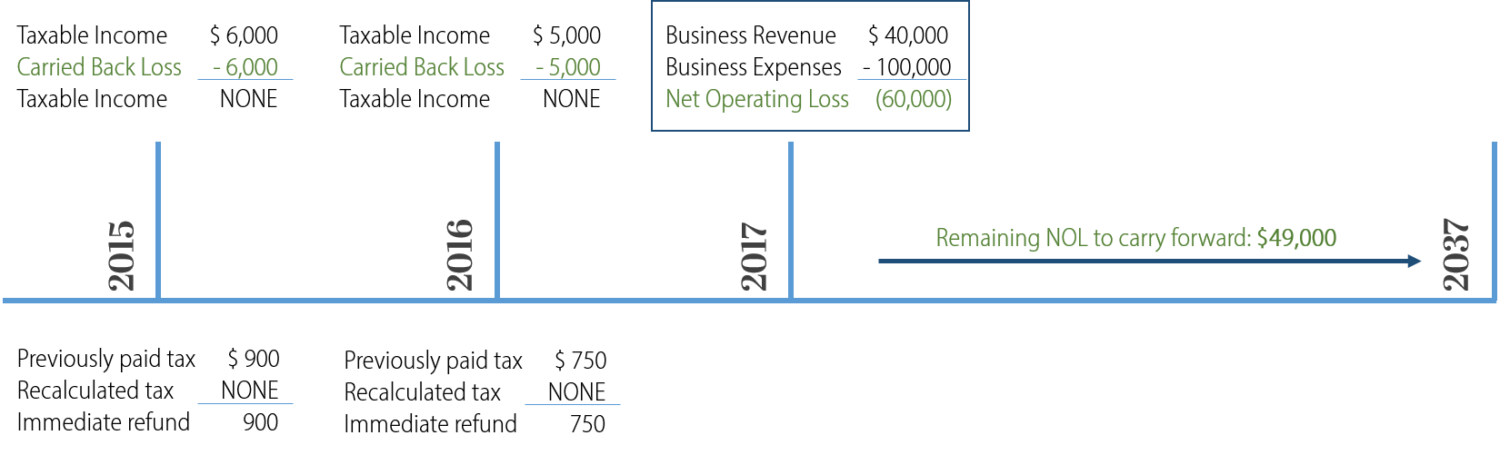

Say your business incurs a $60,000 NOL for the 2017 tax year. You could choose a carryback period for this NOL of two years preceding the lost (first to the earliest year) and then carry forward any remaining amount for up to 20 years after the year in which it incurred the loss. So you might elect to carry back the entire loss first to 2015. If your 2015 net income was $6,000, you could use $6,000 of the NOL to offset this income and receive a refund of the tax you previously paid on that income.

From there, you'd have $54,000 of remaining NOL to apply to the 2016 tax year, after which you'd have the amount unable to be absorbed by 2016 income to carry forward to 2018 and beyond, until the NOL is fully absorbed (or until you hit the 20 year mark).

Best way

This is just one example of how the NOL deduction might work for you. To get a better grip on the best way to handle it, please give us a call.