National Estate Planning Awareness Week is finally here, offering the perfect opportunity to reflect upon some of the increasingly important topics- such as the impact proper estate planning can have on your income tax bill.

As the gift tax and estate tax exemption has significantly increased, and the estate tax rate has decreased, individual income tax and capital gains tax rates have increased. This means that those who expect to have little or no estate tax liability should shift their focus and strategies for reducing income taxes.

Taxpayers, including individuals, estates, and trusts, face a top income tax bracket of 39.6%. For taxpayers subject to the Affordable Care Act's net investment income tax (NIIT), add an additional 3.8% to that. Don't forget state income tax, with rates that can run as high as 12% in some states. This results in a combined income tax rate that can eclipse 55% for some taxpayers. These startling rates leave taxpayers asking what they can do about it.

There are a number of sophisticated tax planning ideas, but for our purposes today, we're going to stick to the basics. They key element is understanding your income level, tax rates, and available options. Additionally, the large gift and estate planning exemptions allows for flexibility to gift among family members and integrate trust planning into your annual tax planning conversation.

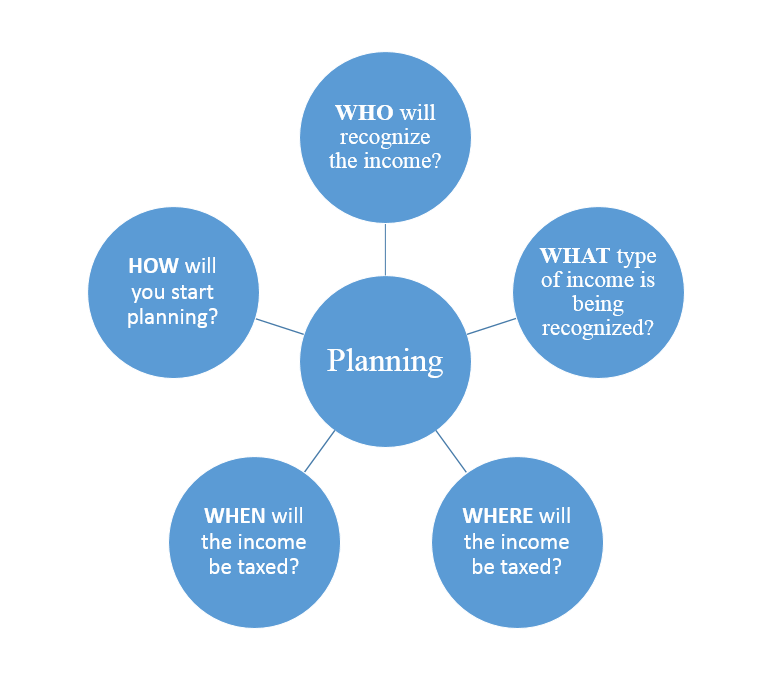

To get the most out of this planning conversation, the who, what, where, when, and how of planning are simple questions you can discuss with your tax advisor during the planning process. Specifically these represent:

- The who: Who will recognize the income? Do your children (or grandchildren) have a lower tax bracket? An estate or trust reaches the maximum tax rate at $12,300 of income. Distributions can move this income to lower tax bracket individuals.

- The what: What type of income is recognized? Distributions from an IRA are taxed at ordinary rates whereas long-term capital gains are taxed at a flat 15 or 20%. Knowing your options will help with your decisions.

- The where: Many states have different rules when taxing individuals, estates, and trusts. Where the income ultimately gets taxed can save taxpayers up to 12% annually.

- The when: They say timing is everything and taxes are no different. Spreading income over multiple years or matching deductions appropriately can save real tax dollars.

- The how: Remember, you're not in this alone. Consult with your tax advisor today and get started!

Michael Deering is a tax partner at Mowery & Schoenfeld who specializes in estate and gift planning and taxation. He serves as the Director of Taxes. He is the immediate past-chair of the Illinois CPA Society's Estate and Gift Committee and also participates on the Board of the Chicago Estate Planning Council