Part 3: ASC 842 is coming. Read on to learn about how to calculate your lease liability under the new standard.

Please note, if applicable, your M&S Advisor will reach out soon to ensure the implementation of this standard.

The New Lease Standard...Coming (really) soon!

You’ve probably heard rumblings about the FASB’s new accounting and reporting standard for leases – Accounting Standards Update No. 2016-02, Leases (Topic 842). This new standard will become effective for non-public business entities for fiscal years beginning after December 15, 2021. This standard requires companies to include more leases than ever on their balance sheet.

For many of our clients, implementation may require significant investment(s), attention, and leadership time.

In our previous article, "New Lease Standard is Coming (really) soon!" we covered the basics of the analysis and accounting behind the new standard. Last week, we dove in even deeper to help you identify "Operating Leases affected by ASC 842".

Today we will dig into the ins and outs of calculating your lease liability under ASC 842.

Calculating lease liability

Now that we have used the lease test to identify operating vs. finance leases, it’s time to calculate the "right-of-use asset" and lease liability that will be included on the balance sheet. The lease liability is equal to the present value of the remaining lease payments. To determine this:

- First, determine the lease term.

- Next, calculate the total lease payments over the lease term.

Finally, discount these payments using the appropriate discount rate to calculate the present value.

How do I calculate the lease term?

As noted above, the first step in calculating the lease liability, is to determine the term of the lease. The term is the total amount of the time between the commencement date and the ending date of the lease. The term may include periods covered by a renewal option, if it is reasonably certain a renewal option will be exercised.

How do I calculate the lease payments?

Next, we need to calculate the lease payments. In order to do this, we must break down the components of the lease agreement to understand what to include and what not to include. Once we have identified all of the lease components, we must then determine which will be included and those we will ignore in our calculation. And, finally, we perform the actual calculating!

Let’s break down the components of the lease agreement.

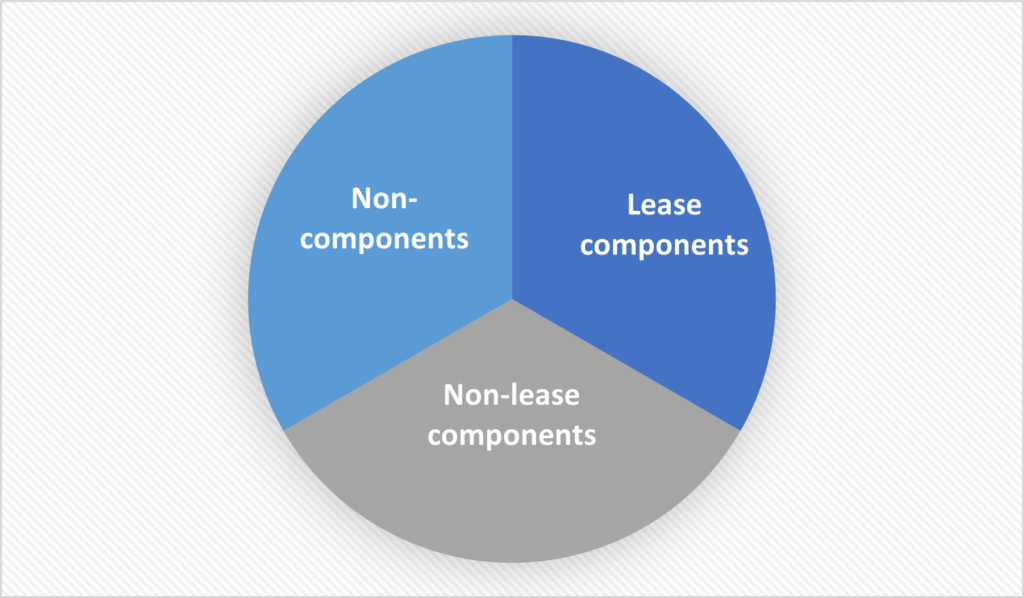

Lease Components:

The entity shall consider the right to use an underlying asset to be a separate lease component if both of the following criteria are met:

- The lessee can benefit from the right to use

- The right to use is not highly dependent on or highly interrelated with other right(s) of use

Non-Lease Components:

Components of a contract include only those items or activities that transfer a good or service to a lessee. An example of a non-lease component in a contract might be charges for common area maintenance.

ASC 842 requires lessees to allocate the consideration in the contract to the lease and non-lease components.

- The lease components are included in the lease payment calculation

- The non-lease components are excluded in the lease payment calculation

Non-Components:

What about other items noted in the lease agreement, such as reimbursements for insurance or administrative tasks? According to ASC 842, these are not components of the contract. As such, they should be excluded from the lease payment calculation.

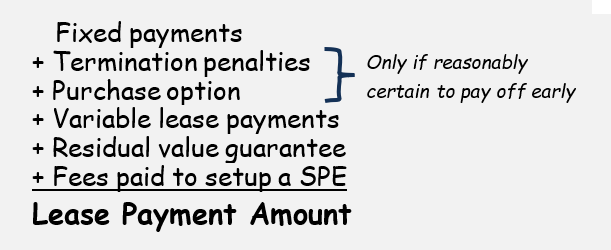

Calculating the Lease Amount

Now that we have identified the different components of the lease payment, let’s calculate the lease amount.

And voila, you're done! If this process leaves you feeling a bit overwhelmed, you are not alone. The new lease standard is complex and full of circumstantial exceptions. Your M&S Advisor is here to help you understand and implement this new change!

YOUR first step...

ASC 842 may impact the debt and credit arrangements you have with your lenders. In fact, while the health of your business may not change – the updates to your financial statements could have a significant and negative impact on your debt ratios. In the most severe cases, this could trigger a “default” on your debt agreements.

In addition to discussing the changes with your M&S Advisor, we recommend reaching out to your lenders and banking partners to discuss how your financial information will be used and what potential impact the new standard will have.

Specially, you and your partner should:

- Review any clauses in your current agreements preventing default from the GAAP adoption

- Renegotiate loan agreements to accommodate the impact of ASC 842

- Obtain an incremental borrowing rate used to calculate the value of your lease and obligations

We are here for you

As things continue to evolve, we will be here to guide you through any changes or questions. Our office has started to reopen. All clients can now safely join us in person or we can meet with you remotely, depending on your preference.