When it comes to retirement planning, you did exactly what you were supposed to do; maximized contributions to your retirement plan, maximized your employer's contribution to your plan, and then let it grow unfettered until retirement. For many, your retirement plan(s) are now the largest asset in your estate, and it has an unenviable built in tax liability. Proper planning can help avoid estate planning traps and minimize your exposure to this tax liability.

As a continuation of our observation of NEPAW, let's take a look at some of the common must do's of estate planning and income tax planning.

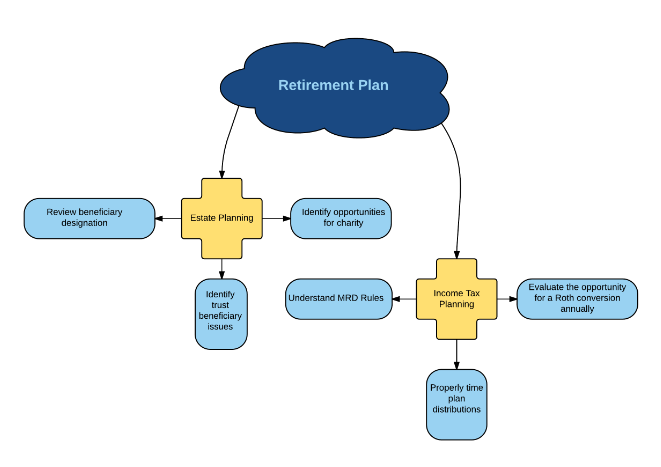

Estate planning must do's:

- Review your beneficiary designation every few years. Make sure your primary and contingent beneficiaries are current.

- If you have charitable intent, retirement plans are a very tax efficient asset. It will be important to clearly identify this in your beneficiary designations.

- If you identify a trust as a beneficiary, you should consult your advisor. This is a very complex area and could result in accelerating income and tax to your beneficiaries if not properly planned.

Income tax planning must do's:

- Understand the Minimum Required Distribution (MRD) rules. Know when they start and how much to distribute in order to avoid large penalties.

- The benefits of a Roth IRAs are well known: they offer tax free growth vs tax deferral, and don't require an MRD. Roth conversions are a useful tool and opportunities for conversions should be reviewed annually. One of the most comforting features is their reversibility- Roth conversions can be reversed anytime up to the next year's tax filing deadline (including extensions).

- Timing of plan distributions or Roth conversions can also minimize taxes. For example, if a taxpayer incurs a net operating loss or has a large increase in medical bills in a certain year, these deductions can be used against retirement income and reduce the tax impact.

Spending the time now to focus on properly identifying and executing the appropriate planning opportunities can preserve the asset that you worked so hard to accumulate. It is important to address these issues while the planning opportunities still exist- the laws surrounding estate, gift, trust, and individual taxation are always changing.