The PATH Act of 2015, recently signed into legislation by the President, reaches more than just small businesses and their owners; there are provisions made permanent by this act that will affect individual taxpayers, too.

What is the IRA Charitable Rollover Provision?

The IRA charitable rollover provision allows taxpayers to exclude up to $100,000 annually of qualified charitable IRA distributions from gross income. This makes funding contributions with IRA distributions very appealing to those who are subject to minimum required distributions. See, the provision allows for 100% of the amount that is required to be distributed and would have been subject to tax to instead be donated to charity, thereby avoiding 100% of the potential taxation.

What is a "Qualified Charitable Distribution" from and IRA?

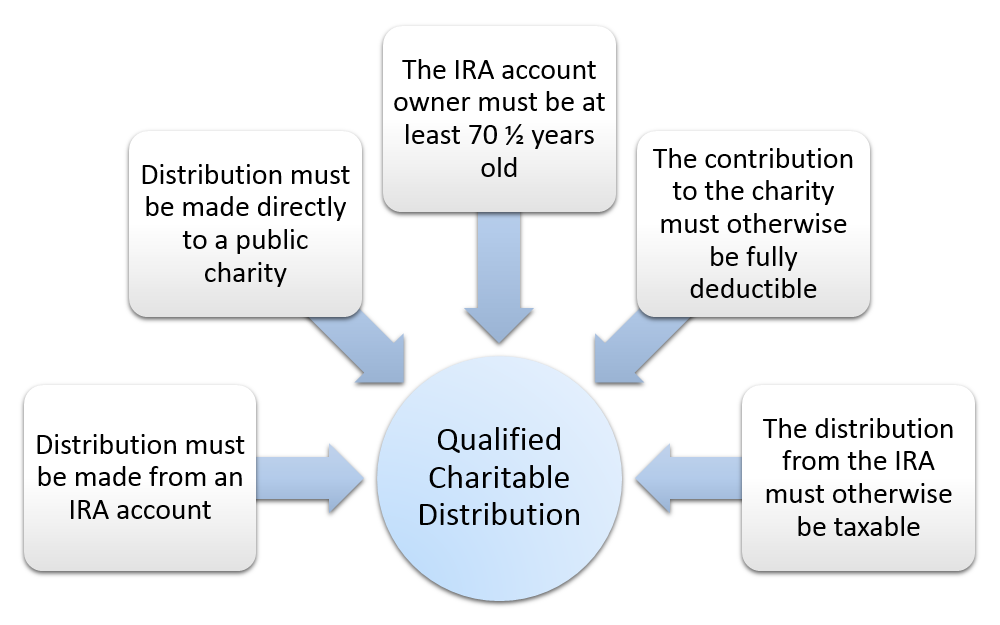

There are a total of 5 requirements that make a distribution a "qualified charitable distribution." These include the following:

- The distribution must be made from and IRA account. This does not include distributions from SEPs, SIMPLE plans, §403(b) plans, §401(k) plans, profit sharing plans, or pension plans. Funds from these accounts can be rolled over into a qualifying IRA account, however.

- The distribution must be made directly to a public charity. Public charities generally include churches, hospitals, museums, and educational organizations. Donor-advised funds operated by public charities, split-interest trusts, and non-operating private foundations, however, do not qualify. Also, funds must be made explicitly payable to the charity; funds transferred to the account owner and then endorsed to the charity will not qualify.

- The IRA account owner must be at least 70 1/2 years old.

- The contribution to the charity must otherwise be fully deductible. If there is any benefit to the taxpayer, such as FMV of a dinner or property received, the entire contribution will be disqualified from this provision.

- The distribution from the IRA must otherwise be includible in gross income. Only the taxable portion of the distribution qualifies under the provision.

What Can I Do Now?

This provision has been retroactively extended to include all distributions made from an IRA account from January 1, 2015 on forward. To receive the tax benefit for 2015, however, all charitable gifting must be done by December 31, 2015; this means that while there is still time for planning, there isn't much of it. You can work with your advisor to determine how to best take advantage of these recently extended benefits.