The net investment income tax (NIIT) can catch you by surprise if you’re not aware of the thresholds. Higher-income homeowners, sellers of second homes, and investors recognizing significant gains should be aware of when the NIIT applies and how to avoid or reduce it to maximize their tax efficiency and pass on more of their wealth to their loved ones.

However, many homeowners and sellers still get caught off guard because they have cleared traditional tax hurdles, such as capital gains rates, but have overlooked the NIIT. It’s essential to remember that the NIIT is its own tax with its own rules.

What is the Net Investment Income Tax (NIIT)?

The NIIT is a 3.8% tax on certain net investment income for individuals, estates, and trusts. Capital gains, interest, dividends, rents, and royalties count as net investment income, while several types of income are excluded, like active business income and wages. It also applies to income from businesses involved in trading financial instruments or commodities and businesses that are passive activities to the taxpayer.

When Does Net Investment Income Tax Apply?

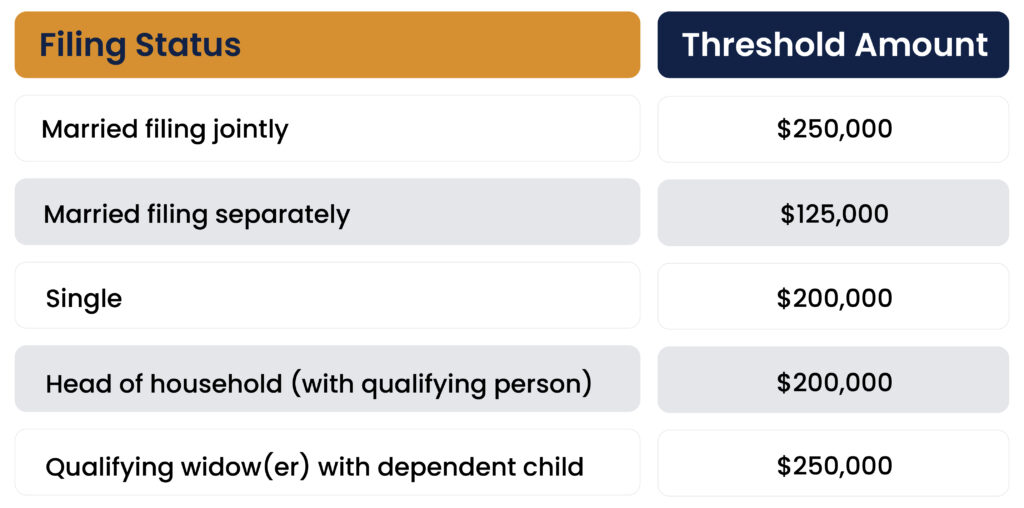

The NIIT applies to taxpayers in the following thresholds:

Nonresident aliens, dual-status, and dual-resident people have different rules, making working with a tax advisor helpful in these cases to avoid paying more taxes than necessary.

How the NIIT Is Calculated

For the purposes of NIIT, your modified adjusted gross income (MAGI) comes into play. It refers to adjusted gross income (AGI) increased by the difference between “amounts excluded from gross income under section 911(a)(1) and the amount of any deductions … or exclusions disallowed under section 911(d)(6) for amounts described in section 911(a)(1).“ For those that live and work abroad, you’ll also need to add back the foreign earned income exclusion..

The tax applies to your net investment income or the excess of your MAGI over the threshold, whichever is less. For example, if a married couple has MAGI of $350,000, including $75,000 of net investment income, the tax is 3.8% of $75,000. Wealthy taxpayers may not feel the impact of the NIIT most years, only to unexpectedly be pushed into NIIT by the sale of their home.

What Types of Home Sales Can Trigger the NIIT?

In general, the net investment income tax only applies to gains that are actually taxable. If part of your home sale is excluded from income for regular tax purposes, that portion is also off the table for NIIT. That’s where the Section 121 exclusion is beneficial.

When you sell your primary residence and qualify for the Section 121 exclusion, you can exclude up to $250,000 of gain (or $500,000 if you’re married filing jointly). That excluded amount isn’t included in your gross income, and because of that, it won’t be subject to NIIT either.

The NIIT can be triggered by the following types of home sales:

- Primary residence (with and without full exclusion)

- Second homes and vacation homes

- Investment and rental properties

To qualify for the Section 121 exclusion, you must meet these requirements:

- You have owned the home for two of the five years ending the date of the sale.

- You have used the home for at least two years in the same five-year period. The two years don’t need to be consecutive. You also can’t use this exemption more than once every two years.

There are some exceptions to the two-year rule, too. You can get a partial prorated exclusion for a job change, health reasons, and other qualifying events. Non‑primary residences don’t qualify for an exclusion.

Practical Strategies to Reduce or Avoid NIIT

If your home sale will trigger the NIIT, whether that’s because the gain will exceed the exclusion amount or because the home isn’t your primary residence, the following strategies can help reduce or eliminate the tax:

- Tax‑loss harvesting: If you have any stocks or investments that have declined in value, you can consider selling them to generate losses you can use to offset the gain.

- Basis planning: Because the NIIT applies to profit and not gross proceeds, keeping track of your home improvements can help you reduce or avoid the NIIT.

- Timing the sale: By strategically selling in a lower-income year or spreading out transactions, you may be able to keep your MAGI below the thresholds and reduce or avoid NIIT.

- Converting a second home to a primary residence: If making your second home your primary one is feasible, this can help you pay a partial net investment income tax in most cases.

- Charitable giving or retirement planning: Certain donation and retirement strategies can help reduce MAGI.

For these strategies to work, planning should happen before the home sale, not after, because once the transaction closes, most of the tax outcomes are already locked in.

Common NIIT Misconceptions

Common misunderstandings about net investment income tax rules can result in you having to pay the tax. One of the biggest is assuming that if you use your exclusion on the gain for regular tax purposes, NIIT will never apply. While the excluded gain itself is not subject to NIIT, any portion that remains taxable can still trigger it.

Another misbelief is that only traditional investment properties are subject to NIIT. However, the tax can apply to gains from many sources, including second homes or even partially taxable sales of a primary residence.

It’s also a mistake to think of NIIT as a one-time issue. Instead, NIIT is driven by your overall income level and investment activity each year and should be considered as part of your yearly tax planning process.

Key Takeaways for Home Sellers

For high-net-worth families who want to be tax efficient, planning ahead is crucial. Remember that NIIT can still apply even with the home sale exclusion, and your higher-income years increase your risk of exposure to this tax. Working with an advisory team helps you significantly reduce your tax burden and align your plans with other aspects of your financial picture.