Many businesses are focused on succession planning, which involves transitioning the ownership from or reducing the involvement of the founders of the company in anticipation of their retirement. One strategy is to transfer business to the next generation of family members. This can be done gradually over a period of years through gifting or all at once through an outright sale of all or a portion of business ownership. One potential strategy is a family limited partnership (FLP).

FLP's are frequently used to move business interests to the next generation. The entity is typically a limited partnership consisting of general partners (GP's) or limited partners (LP's). One or more GP's are responsible for managing the FLP and its underlying investments. LP's have an economic interest in the FLP; however, the LP's interests generally lack control and marketability. All control and management of the FLP is vested in the GP's.

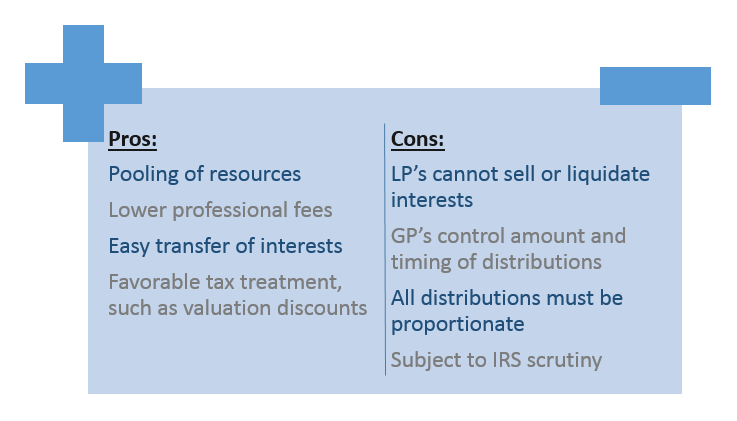

Benefits:

FLP's hold investments such as business interests, real estate investments, and publically traded or privately help securities contributed by the GP's and LP's. FLP's have several benefits. They allow family members with aligned interests to pool resources, thus lowering legal, accounting, and investing costs. They allow one family member (who is generally the GP) to move assets through transfers of LP interests to other family members while retaining control over the assets.

FLP's also allow for favorable tax treatment relating to the transfer of the assets. Family Limited Partnership FLP Benefits and RisksFor these purposes, the value of the partnership interests transferred can be discounted for factors such as lack of control and lack of marketability. A lower valuation can minimize the potential gift taxes and income taxes related to the transfer, therefore it is worth obtaining a formal valuation by a professional appraiser to establish the value of the underlying assets and partnership interests.

Risks:

Some drawbacks to FLP's include how they are structured. For example, LP's cannot sell or liquidate their LP interest and the timing and amounts of cash distributions are controlled by the GP. Additionally, a distribution cannot be made to one of the partners unless all partners receive their proportionate share of the partnership distributions.

They can also result in exposure to IRS scrutiny; the agency often challenges FLP's it believes are invalid. These challenges arise because taxpayers do not follow proper procedures in establishing the FLP. For instance, the FLP might make disproportionate distributions to GP's- the result of this is that the value of the FLP can be included in the estate of the GP when he dies.

If the rules are closely followed and the risks carefully understood, however, the use of an FLP can be a very effective tool in succession planning.